21 Avenue de la Gare: The Financial Heart of a Meat Empire

JBS is the world’s largest meat company — and runs its financial operations out of Luxembourg. At a recent conference we co-organized in the Grand Duchy, researcher Maarten Hietland presented findings from his studies for World Animal Protection and SOMO (Centre for Research on Multinational Corporations), on how exactly this works. Here, he summarizes the research.

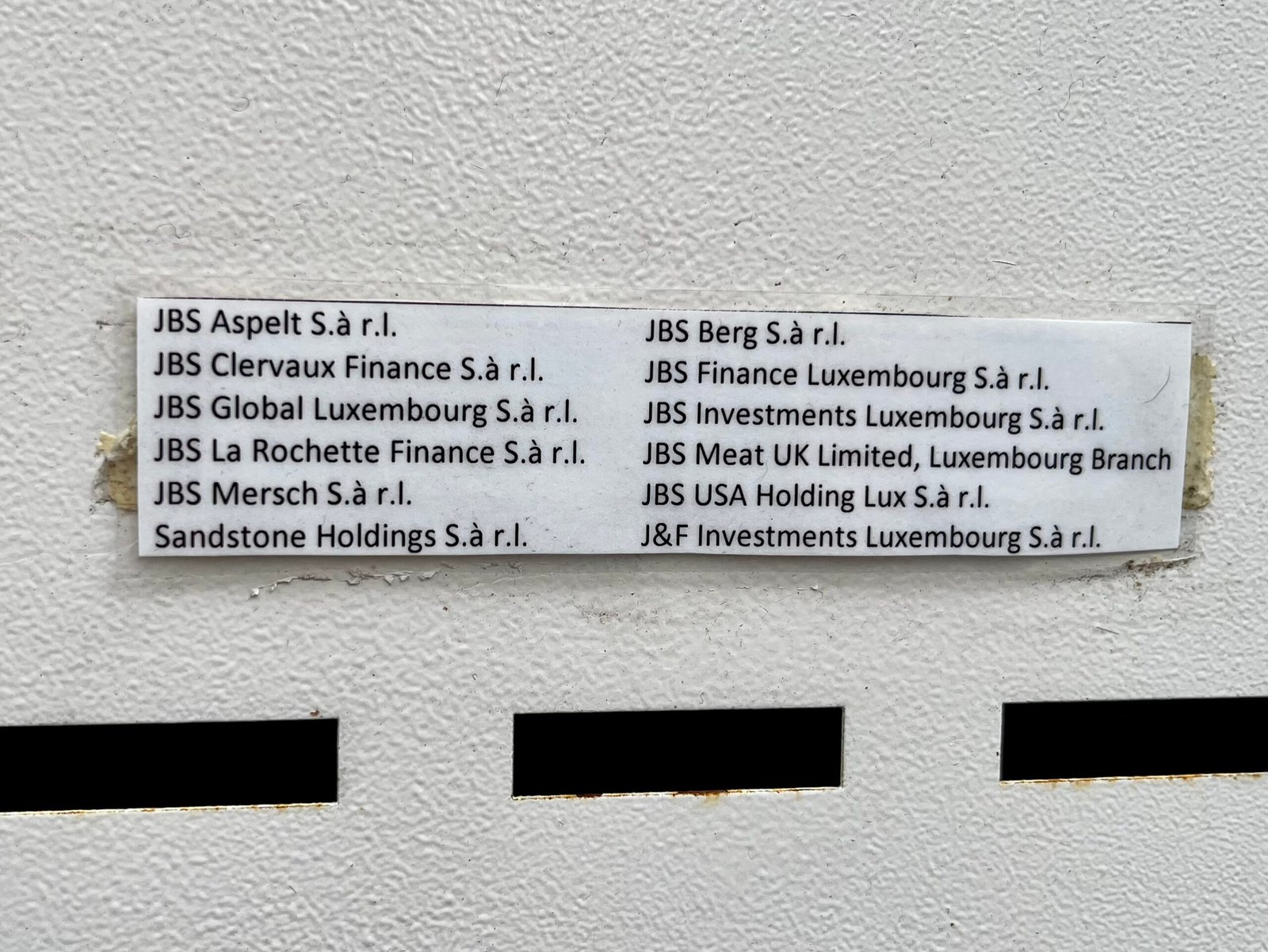

JBS is the world’s largest meat company.1 Most of its activities, being the slaughtering and processing of livestock, take place in Brazil and North America. The financial heart of this company, however, is located at 21 Avenue de la Gare, right in the center of Luxembourg City. People who pass by this building will not see any physical traits of the world’s largest meat company, except for a letterbox with its logo. JBS does not conduct any actual economic activities in the Grand Duchy.2 Nonetheless, there are currently at least 11 JBS subsidiaries in Luxembourg — staffed by a mere five employees — providing JBS with the financial basis to slaughter and process 75,000 cows, 14 million chickens, and 115,000 pigs. On a daily basis.3

JBS’s business has been closely tied to serious human, environmental, and animal rights violations. The company has built its meat empire through unethical practices, including illegal deforestation, the destruction of Indigenous lands, modern slavery in its supply chains, corruption and dangerous working conditions that contributed to COVID-19 deaths and other injuries. It also has a troubling record of animal welfare abuses. Rather than reform, JBS has largely continued these practices by paying government fines and settlements, treating them as a cost of doing business.4

We need to go back in time to understand the role of Luxembourg regarding JBS. JBS was founded in 1953 in Brazil by José Batista Sobrinho as a local company (the name comes from the founder’s initials). His sons, the so-called ‘Batista brothers’, coordinated the spectacular growth of the company, from the early years of the 21st century onwards until now. One of the milestones took place in 2007, when the company became publicly listed in Brazil and started to grow its business internationally through various acquisitions.5 But things needed to go more efficiently. In the summer of 2015 it was decided by both PWC and the directors of the company that JBS needed to redefine its corporate structure in order to create a group structure that would allow for the (tax) efficient movement of funds around the group, the (tax) efficient repatriation of funds to Brazil, and the possibility of an initial public offering in the US. The project that involved Luxembourg was named GRAP: Global Regional Alignment Project. According to PWC, the restructure was expected to save US$250 million in US tax and potentially US$70 million per year in Australian tax on (then) future profits.6

JBS engaged with a whole team of advisors, including PwC in Brazil, the United States, Australia, Ireland, the United Kingdom, the Netherlands and Luxembourg.7 By the end of 2015, JBS had 16 Luxembourg-registered subsidiaries.

The research performed by SOMO8 and WAP9 is based on the analysis of the financial statements of all the JBS subsidiaries that have been incorporated in Luxembourg: at least 23 different entities throughout the period 2015-2024.10 Its presence in Luxembourg serves solely corporate structuring purposes. The subsidiaries in Luxembourg are at the heart of JBS and have financial connections with the most important JBS subsidiaries worldwide: in Brazil, the United States, Canada, Mexico, Australia, Ireland, the United Kingdom, the Netherlands and Malta.11 And these financial connections are substantial. Take, for example, the Luxembourg-registered “JBS Holding Luxembourg S.à r.l.”: its 2022 financial statements show that the equity value of a subsidiary operating in the Netherlands and Australia exceeds US$17 billion. The main reason for the use of Luxembourg, as was also mentioned by PWC in the Australian court case, is the avoidance of taxes. JBS has been extremely successful in that regard. Between 2019 and 202212, a net amount of US$0.5 million of corporate income tax has been collectively paid by JBS subsidiaries in Luxembourg, while the Luxembourg-based entities collectively recorded US$3 billion in pre-tax profits. That implies a staggering effective corporate income tax rate of less than 0,02%.13 We have identified multiple mechanisms through which the Luxembourg-based JBS subsidiaries have played a key role in reducing the group’s corporate tax liabilities on its global profits.

Debt-interest: Luxembourg serves as a central hub in JBS’s internal financing system. In 2022, its Luxembourg subsidiaries received nearly US$22 billion in loans provided at near–zero interest rates from low-tax jurisdictions such as Malta and Delaware. At the same time, they issue high-interest loans to JBS’s operating companies in Brazil, the USA, the UK, Ireland, Australia, and Mexico. The resulting high interest costs lower the tax burden in these production countries, while the corresponding interest income is taxed only minimally in Luxembourg. In this way, JBS shifts profits into a low-tax environment through its Luxembourg entities.14

Profits-Dividend: Intercompany dividend flows to and from subsidiaries are one of the main ways for multinational companies to redistribute profits generated by their operations worldwide. Many countries levy a withholding tax on outgoing dividend payments to foreign entities. To avoid such tax liabilities, many multinationals structure dividend payments and other financial flows through holding companies in countries with favorable international tax treaties and favorable domestic tax legislation. These jurisdictions generally do not levy a withholding tax on intercompany dividend payments and do not tax dividend collections received from abroad. Luxembourg has a vast network of international tax treaties with many countries. One of the effects of many of these treaties is to reduce the amount of withholding tax the treaty-partner countries can charge on intercompany dividend payments being remitted to Luxembourg, in some cases to zero percent. At the same time, Luxembourg’s domestic tax legislation does not impose withholding tax on outgoing dividend flows to foreign entities. This creates the perfect context for dividend withholding tax avoidance. Analysis of available financial statements of JBS’s companies in Luxembourg shows that significant dividend flows from its global operations are routed via its subsidiaries in Luxembourg. Between 2019 and 2022, almost US$11 billion in intercompany dividends flowed through JBS’s group of Luxembourg subsidiaries, thereby avoiding withholding taxes on these dividend flows. It appears Luxembourg is being used as a central hub to redistribute worldwide profits to where capital is needed (either for investments or for the ultimate owners).15

The above research shows the importance of Luxembourg for JBS. If Luxembourg did not permit JBS to make use of its favorable tax regime, the company would have to pay much more taxes in the countries where the company operates. And this tax revenue is essential for governments to fund health care, education and infrastructure. It is time for Luxembourg to close the loopholes that allow companies like JBS to erode tax bases worldwide while profiting from environmental destruction and human rights abuses.